CERF Blog

National Markets:

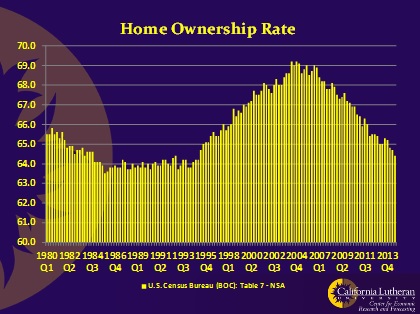

Since the recession began, we’ve said that residential real estate markets would not recover until the homeownership rate (the percentage of households owning the home they live in) fell to the 64 percent to 65 percent range. We also said that residential markets would recover when the homeownership rate fell to that range. We may have been wrong about the second part.

Before we get to the why we may have been wrong, we need to be clear on what a recovery looks like. We consider a recovery to be when normalized housing starts are near normal. That is, when housing starts per thousand population approach their long-run average.

Well, the homeownership rate is well within the range where we expected recovery:

However, contrary to our expectations, the decline in the homeownership rate doesn’t appear to be slowing down. There is not even a hint in the data that the decline won’t continue. It appears that a sub-64-percent homeownership rate is rather likely.

Even worse for our forecast, normalized housing starts are not approaching the long-run average. It’s worse than that. Normalized housing starts haven’t recovered to even the lowest levels observed before this recession:

Housing starts, while improving, are dismal, and the homeownership rate continues to decline. What is going on here? Why were we apparently wrong?

I think we did not critically examine a key assumption. We assumed that the post-recession or post-recovery economy would be much like the pre-recession economy. It’s not.

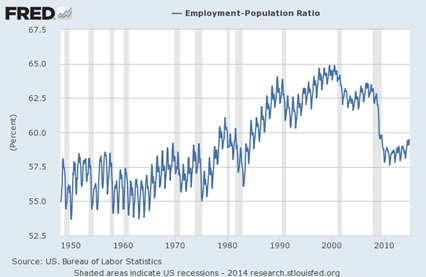

A lower percentage of our population is working:

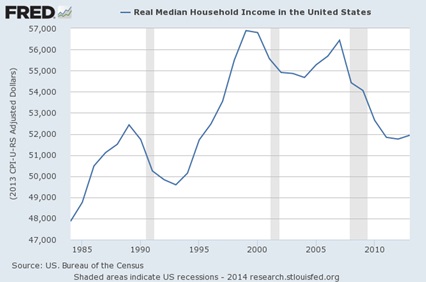

The real median income is way below pre-recession levels:

More working people are working part time:

Birth rates are down. Marriage rates are down. Our young people are having trouble starting their careers.

All this adds up to lower demand for home ownership. This means that the stable homeownership rate is probably lower today than it was prior to the recession. It’s lower than the 64 percent to 65 percent that we anticipated would herald a robust recovery in residential prices.

Some will think that our analysis is excessively negative. They will point out that prices have increased over the past couple years, and sales were up. This is true, but the demand was mostly from investors, often institutional investors, because of higher rents. That has mostly played itself out, and the price increases have slowed while sales volume appears to have softened.

We think the institutional investor provides a floor for residential prices, but a robust market will need traditional sources of demand. These are an increasing population of new market entrants: young people establishing households and families.

So, what homeownership rate will accompany a robust residential market recovery? We don’t know, and determining that rate in a world changing as rapidly as ours is changing is a non-trivial problem. We are working on it, but at this point, we can’t confidently assure readers that we will have it anytime soon.

California Markets:

California sales and prices show signs of weakening, but all markets are local.

In general, luxury markets are doing quite well. The declining median income means that wealthier people have a higher proportion of our income, which increases demand for luxury homes. It is also true that California’s luxury markets are partially insured against the local economy. These are world markets, and the world has large numbers of wealthy people who would like to live in California.

Lower-end and inland home markets are much weaker. At this point, it is difficult to be optimistic about prices or volume.

Apartments continue to be a strong market, as has been the case throughout the recovery. Indeed, most new California residential units being built are apartments. Because we’ve seen no sign of weakening rents, and because new construction is so difficult and time consuming, apartments will likely remain strong throughout 2015.